Can You Negotiate Settle Private Student Loans?

Looking for trusted legal experts to handle your case? Whether it’s a complex claim or a personal issue, FreeLegalCaseReview offers free consultations and expert advice tailored to your needs. Or call us directly at 833-248-4565.

Understanding Settle Private Student Loans can be daunting, yet it is essential for borrowers seeking debt relief. Unlike federal loans, private loans have varied negotiation options. Many borrowers have successfully settled their loans for less than owed, particularly during financial hardship. This approach can be beneficial if you struggle with payments or are considering bankruptcy. Here are some key insights for negotiating your private student loan settlement:

- Assess Your Financial Situation: Review your finances to understand your budget and what you can afford, strengthening your negotiating position.

- Contact Your Lender: After assessing your finances, reach out to your lender. Be honest about your struggles and express your desire to settle the loan.

- Propose a Settlement Amount: Suggest a specific settlement amount lower than your total balance but reasonable enough for the lender to consider.

- Get Everything in Writing: If a settlement is agreed upon, ensure you receive the terms in writing before making any payments to protect yourself from future claims. Real-world examples illustrate that borrowers with a clear plan often achieve better results.

For instance, one borrower settled a $30,000 loan for $15,000 after proving financial hardship. Another individual, facing foreclosure, found that hiring a lawyer not only helped with their mortgage but also provided insights into settling student loans. Negotiating may be challenging, but it is a vital step toward regaining financial control.

The Process of Negotiating Private Student Loan Settlements

Negotiating private student loan settlements can seem intimidating, but it is a practical option for many borrowers. The first step is to assess your financial situation and gather essential documentation, such as loan details and income statements. With this information in hand, you can approach your lender to explore settlement options. Lenders are often open to negotiation, especially if they sense you may default on your loan. Here are some key steps to follow when negotiating your private student loan settlement:

- Assess Your Financial Situation: Determine what you can realistically afford to pay.

- Contact Your Lender: Reach out and express your intent to negotiate, being honest about your circumstances.

- Make an Offer: Suggest a settlement amount that is lower than your total debt.

- Get Everything in Writing: Ensure you receive written confirmation of any agreement reached.

- Consider Legal Help: If negotiations become complicated, seeking advice from a lawyer specializing in debt settlements can be beneficial.

Real-world examples show that negotiating private student loan settlements can yield positive results. For instance, a borrower with a $50,000 debt settled for $30,000 after proving financial hardship. This not only alleviated their debt but also improved their credit score. Many have successfully settled credit debt similarly, proving that with persistence and preparation, favorable outcomes are achievable. The potential benefits of settling your loans can lead to a fresh start and significant financial relief.

Key Factors Influencing Private Student Loan Negotiations

Many borrowers of private student loans often wonder if negotiating settlements is possible. The answer is yes, but several key factors can influence the outcome. Understanding these factors can help you approach negotiations with confidence. First, consider the lender’s policies; some are more flexible, especially if they believe settling is preferable to pursuing collections. If you are experiencing financial hardship, communicate this clearly during negotiations.

Your payment history is also significant. Consistent payments may make lenders less inclined to negotiate, while missed payments or being in default can provide you with more leverage. Gathering documentation that supports your financial situation, such as income statements or proof of unemployment, can strengthen your case for a settlement. Here are some additional insights for negotiating private student loan settlements:

- Timing is crucial: Start negotiations early for better outcomes.

- Know your options: Research potential settlement amounts and be ready to discuss them.

- Consider professional help: Consulting a lawyer for foreclosure house issues or a debt settlement expert can offer valuable guidance.

By understanding these factors and preparing effectively, you can enhance your chances of successfully settling your private student loans.

Common Myths About Settling Private Student Loans

Many borrowers mistakenly believe that settling private student loans is impossible, but this is a common myth. In reality, negotiating a settlement can be a viable option, especially during financial hardship. Lenders may accept a lower amount than owed if they suspect a borrower might default, creating a win-win situation. Here are some key insights about settling private student loans:

- Flexibility: Private lenders often have more flexible policies than federal loans, making negotiations possible.

- Financial Hardship: Demonstrating financial hardship can encourage lenders to negotiate. Providing documentation can strengthen your case.

- Real-World Examples: Many borrowers have successfully settled their loans for much less than owed.

For example, one borrower settled a $30,000 loan for $15,000 after months of negotiation, proving that persistence pays off.

If you’re considering settling your loans, follow these steps:

- Assess Your Financial Situation: Know your budget and what you can realistically offer.

- Contact Your Lender: Discuss your situation and express your desire to negotiate a settlement.

- Get Everything in Writing: Ensure you receive written confirmation of any settlement to avoid future disputes.

Steps to Prepare for Negotiating Your Student Loan Settlement

Negotiating a private student loan settlement can be intimidating, but with proper preparation, you can achieve a favorable outcome. Lenders often prefer to settle rather than engage in lengthy collection processes, giving you a chance to negotiate. Start by gathering essential documents, such as loan agreements, payment history, and correspondence with your lender, as these will be vital during negotiations.

Next, evaluate your financial situation to determine a realistic settlement amount. This assessment will help you set a budget and provide leverage in discussions. When approaching your lender, clearly communicate your financial hardships, such as job loss or unexpected medical expenses, to humanize your case and encourage consideration of your offer. Here are key steps to prepare for your negotiation:

- Research your lender: Understand their policies and past settlement practices to guide your approach.

- Set a target amount: Aim for a settlement significantly lower than your total debt, ideally around 30 to 50 percent of what you owe.

- Be persistent: Negotiations may take time, so remain firm and communicate your willingness to settle.

- Consider professional help: If negotiations become overwhelming, hiring a lawyer for foreclosure house or a debt settlement expert can provide valuable support.

Following these steps can enhance your chances of successfully settling your private student loans and achieving financial freedom.

How to Approach Your Lender for a Settlement

Managing private student loans can be challenging, especially if you’re struggling to keep up with payments. If you’re in this situation, you might wonder if you can negotiate private student loan settlements. The answer is yes. With the right preparation and understanding of your financial situation, you can approach your lender and potentially reduce your debt significantly.

Here are some steps to consider when negotiating with your lender:

- Gather Your Financial Information: Compile relevant documents, including loan details, income, and expenses, to present a clear picture of your financial situation.

- Research Your Lender’s Policies: Knowing your lender’s policies on settlements can help, as some may be more open to negotiations than others.

- Prepare Your Proposal: Be ready to explain your reasons for seeking a settlement, emphasizing any financial hardships like job loss or medical expenses.

- Be Persistent and Patient: Negotiations can take time, so don’t be discouraged if the first conversation doesn’t go as planned. Keep communication open and follow up regularly.

Many borrowers have successfully settled their private student loans for less than owed. For example, one borrower negotiated a 50 percent settlement after demonstrating financial hardship, relieving their debt burden. Consulting with a lawyer for foreclosure issues or a financial advisor can also help you make informed decisions. By following these steps, you can effectively settle private student loans and regain control of your financial future.

What to Expect During the Negotiation Process

Negotiating private student loan settlements can be a game-changer, especially when you know what to expect. Start by gathering all relevant information about your loans, such as the total amount owed and interest rates. This preparation gives you leverage during discussions with your lender, who often prefers to settle rather than incur collection costs.

Here are some key steps to follow during the negotiation process:

- Research Your Options: Look into various settlement options before starting negotiations.

- Contact Your Lender: Reach out and express your desire to negotiate, being honest about your financial situation.

- Make an Offer: Propose a settlement amount you can afford, keeping in mind that lenders may counter your offer.

- Get Everything in Writing: Ensure you receive written confirmation of any agreement reached.

- Consider Legal Help: If negotiations get complicated, consulting a lawyer for foreclosure house or debt settlement can be beneficial.

Many borrowers have successfully settled their loans for less than owed. For example, one borrower settled a twenty-thousand-dollar loan for twelve thousand after proving financial hardship. With patience and persistence, you can also achieve a favorable outcome in settling private student loans.

Ready to connect with top legal professionals? Get immediate support— Call us at 833-248-4565.

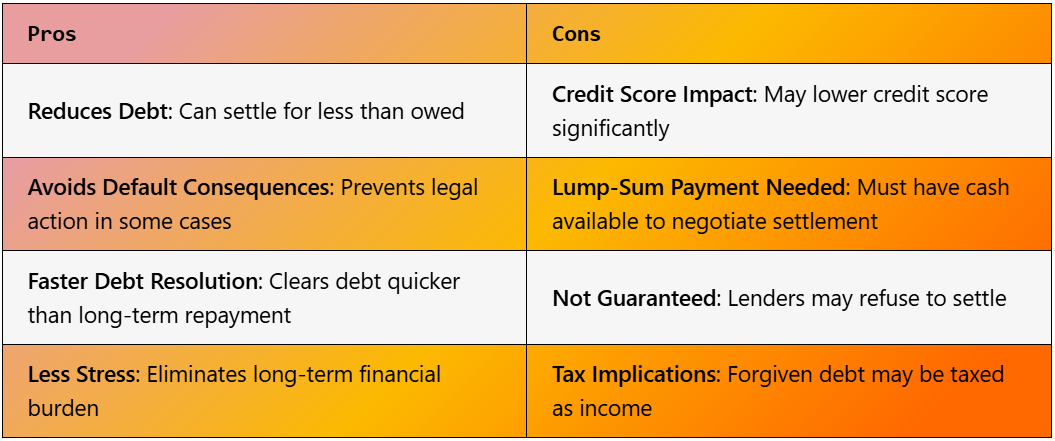

Potential Benefits of Settling Private Student Loans

Managing private student loans can be daunting, but many borrowers may not realize that negotiating settlements is a viable option. Settling private student loans can provide significant financial relief, allowing you to reduce the total amount owed and regain control of your finances, especially during times of financial hardship. Here are some key benefits of settling your private student loans:

- Reduced Debt: You may settle for less than the total owed, saving money in the long run.

- Improved Cash Flow: Lower debt can free up funds for essential expenses like housing or healthcare.

- Avoiding Foreclosure: If you risk losing your home, consulting a lawyer for foreclosure house can help you explore options and settle debts before it’s too late.

- Less Stress: Settling your loans can alleviate anxiety associated with overwhelming debt.

To begin the negotiation process, follow these steps:

- Assess Your Financial Situation: Know your financial standing and what you can offer.

- Contact Your Lender: Discuss your situation with your loan servicer and express your desire to negotiate.

- Prepare Your Offer: Present a reasonable settlement amount based on your assessment.

- Get Everything in Writing: Ensure you receive written confirmation of the settlement to avoid future disputes.

Read Also: When Should You Hire a Foreclosure Defense Lawyer?

Risks Involved in Private Student Loan Settlements

When contemplating the settlement of private student loans, it’s crucial to grasp the associated risks. While negotiating a settlement can alleviate overwhelming debt, it may also lead to negative consequences. For example, settling a loan can adversely affect your credit score, making it more challenging to obtain future loans or credit. Lenders might report the settled amount as ‘settled for less than owed,’ which can raise concerns for future creditors. Key risks to consider include:

- Credit Impact: Settling a loan can decrease your credit score, hindering future borrowing.

- Tax Implications: The IRS may view forgiven debt as taxable income, resulting in unexpected tax liabilities.

- Legal Consequences: If in default, lenders may take legal action, potentially leading to wage garnishment or bank levies.

- Limited Options: Settling may restrict your ability to negotiate better terms later on.

To effectively navigate these risks, consulting a lawyer for foreclosure house situations or a financial advisor is advisable. They can clarify your options and the potential outcomes of settling credit debt. While settling private student loans can provide immediate relief, it’s essential to consider the long-term implications for your financial well-being.

Alternatives to Settling Private Student Loans

Managing private student loans can be challenging for many borrowers. While negotiating a settlement may seem appealing, it’s crucial to explore alternatives that offer relief without the risks associated with settling. One effective strategy is loan consolidation or refinancing, which can reduce monthly payments and interest rates, making loans more manageable.

Additionally, contacting your lender to discuss hardship programs can lead to favorable terms without needing a settlement. Seeking professional assistance is another viable option. Hiring a lawyer for foreclosure house issues can be beneficial if you’re facing severe financial difficulties. They can help navigate the complexities of your loans and clarify your rights.

Furthermore, collaborating with a credit counseling service can provide tailored strategies to settle credit debt without harming your credit score. These experts can negotiate on your behalf, potentially securing better terms than you might achieve alone.

Finally, staying proactive in managing your finances is essential. Regularly reviewing your budget, exploring additional income sources, and maintaining open communication with lenders can help you avoid drastic measures like settling private student loans. By implementing these strategies, you can work towards a more sustainable financial future and reduce the stress associated with loan settlements.

Don’t wait to secure the legal representation you deserve. Visit FreeLegalCaseReview today for free quotes and tailored guidance, or call 833-248-4565 for immediate assistance.

You can also visit LegalCaseReview to find the best Lawyer.